How to Build Wealth When the Economic Ladder Is Broken

Build systems that protect you from institutions betting on your failure.

The Complexity Trap: Why Simple Finance Wins in a Complicated World

The Paradox of Progress

As our world becomes more advanced, AI-driven, and resource-rich, life should theoretically get easier. That's the whole point of progress, right?

But the opposite is happening. Your life becomes more complex, more confused - and nowhere is this truer than with your finances.

Gone are the days of walking into banks, depositing money, buying stocks on the trading floor. Everything is now digital, intertwined, and most importantly, accessible. That accessibility helps us move faster and be efficient, but it creates a massive problem: with infinite options comes infinite confusion.

A representation of the old days.

Understanding finances and making the right financial decisions has become one of the most difficult things in the world. As a personal finance content creator, I experience this firsthand every day in my comments section.

Do I invest? Do I just live my life? How do I even start? These questions paralyze people, especially those in their early 20s.

From Transparency to Gamification: How Fintech Changed

Actual definition of FinTech.

When I think about old fintech (the 2010-2015 era) — I think about the early days of Mint. The whole premise was simple: one free service that gave you visibility to your money. You connected your bank accounts and it helped you see where your money was going, what your spending categories were, all in one digestible spot.

Old fintech was focused on transparency. Helping you gain visibility and clarity on your finances, combining all these different accounts into one place so you could understand your financial grounding.

Mint used to be clutch in the past.

Then something shifted.

New fintech (2020 to 2025) became about something completely different: how can you generate thousands or millions of dollars from your phone?

It's aggressive investing, AI-powered trading, cryptocurrency everywhere. It's the gamification of money. How can I buy these coins immediately? How can I invest in these stocks immediately? Even if you don't know how to, is there an AI model to help me do these things?

The focus moved from "understand your money" to "get rich quick."

The Gamification Machine

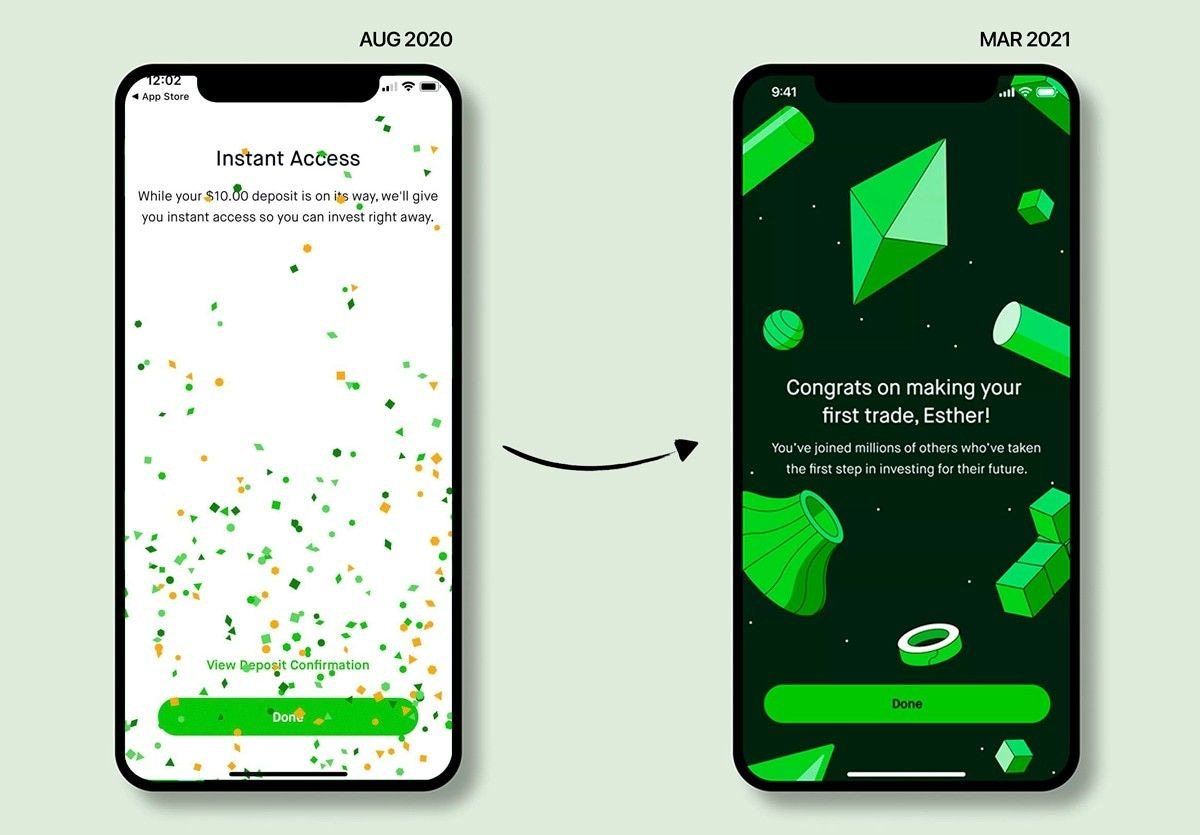

And those “get rich quick” schemes take a whole new level once you gamify money. For example, Robinhood was known for ability to make investing feel like a game.

They're created an engaging cycle. Confetti used to drop from the screen when you would make a purchase. All these things make it feel like a game instead of you actually investing your money.

Before and after of the Robinhood app when a consumer made a purchase.

And don’t get me wrong, I firmly believe you should treat your money like a game sometimes because it keeps you engaged on your path to financial freedom. But the downside is addiction. You become addicted to every trade, every gain, every dollar.

Before you know it, you're no longer investing - you're day trading. You've moved from fundamentals to chasing dopamine hits.

These apps make investing accessible and easy, but they're giving sophisticated tools to inexperienced people who don't understand the severe consequences.

I read about a kid who killed himself because he over-leveraged on Robinhood and assumed he was hundreds of thousands in debt. He wasn't. But the interface, the gamification, the lack of understanding - it all contributed to a tragic outcome.

Why This Is Happening Now: The Perfect Storm

Here's what I've learned about why people make desperate financial decisions. It's not just about being irresponsible. There are real structural forces at play and they're all happening right now.

Force #1: Your Environment Shapes Your Money Mindset

If you're not surrounded by people with money, if you don't learn how they make money and understand how money works in our society, you will view money from a completely different point of view.

If you grow up broke, you view money as evil and the reason for all your problems. If you go to an elite college and see how other people use money, you see it as a form of leverage or time freedom.

I remember when I went to school at Georgetown. It really messed up my mind when I had classmates whose parents would make thousands in a day by doing nothing. And that "doing nothing" was just based off of investing their money - money they already had, money they could afford to let sit and compound.

I would to study in this building, just to end up failing my exam.

Once I learned the power of investing, but more importantly, the power of compounding interest, it was not until then that I really locked in and got my finances together.

But this only changed once I surrounded myself in a different environment. I had to see how wealthy people thought about money to understand it differently. Most people never get that access.

Force #2: The Economic Ladder Feels Broken

Housing is unaffordable. Student loans are crushing. Wages haven't kept up with inflation. The traditional advice of "save for thirty years" doesn't resonate when people feel locked out of the future it promises.

When long-term goals feel out of reach, a zero-day option, a same-game parlay, or a prediction market bet starts to look appealing. Not because it's rational in terms of expected value, but because it provides something that feels scarce: the chance -however small - of changing your financial status.

Or simply put - a chance to skip the broken ladder entirely.

Force #3: The Tools Are There, The Education Isn't

With AI and new technology, everything becomes more accessible. Everyone is finding new ways to help people get better with their money. And remember, the whole idea of advanced technology is to ease people's lives. That's great.

We've been given incredible tools within the fintech space. However, the education part is lacking. People do not know a lot about personal finance. And I think the biggest thing about personal finance is the personal part—the idea of agency, understanding what works for your life and what best makes sense for you.

I was watch a YouTuber called The Daily Driven Porsche. He's an investor who literally only buys dividend stocks and dividend funds. It's not the most efficient way to increase your wealth, but what reassures him every day is the fact that he gets quarterly payouts. He gets that cash flow over and over.

This is his Youtube.

I get it. That works for him. But for me personally, I probably want to get the most returns I can get, so I'll do single stocks or maybe an index fund. He wants the feeling of consistent cash flow, and that's why he does dividend stocks even though they might not produce the highest return.

That's the point. All the technology is out there, but we live in a society where people are unsure of themselves, unsure of their abilities. They lowkey have not taken the time to stick to budgeting, to stick to investing, to stick to saving, and actually see what happens when you do it. Instead, they go from one thing to the next and it jumbles their mind.

The real truth is that you might have a problem with understanding what you want to do with your money.

This Perfect Storm Created the Conditions. Now Make it Worse.

We're glued to our phones, scrolling TikTok, where every other day there's a new 20-year-old millionaire. Gen-Z males' interest in relationships is down, but their urge to gamble is up - sports betting, political betting, options trading.

You see these so-called millionaires and think, "How do I get there?" "Am I behind?"

And those two questions increase the likelihood of gambling, options trading, and risky investing.

The cruel irony: the more information we have, the more difficult it becomes to build wealth.

No one wants to hear the boring thing. They want the complex thing. They think there's some specific trick or hack to build wealth or live the life they want.

It's not true.

We're living in a casino economy—a slot machine where consumers constantly chase the next fix, the next crazy investment that'll change their lives.

Solutions: What You Can Actually Control

Build Your Own Discipline System

Here's the thing about being smarter with money: it's really about being able to regulate your emotions. Not getting overworked, not getting underwhelmed. Taking the highs with the highs, the lows with the lows. Being confident in your investing strategy, your spending journey. You set up a plan and a roadmap to be financially free, stick to it, see it through.

Organic Dreams by Larry June.

Think about it - these millionaires and billionaires have visions so strong that day in, day out, they execute on them. But they don't see the fruits of their labor until 10, 15, 20 years later. That's going to be true for your investments.

But "be disciplined" isn't a strategy. You need systems:

1. Make It Hard to Access Your Money

I remove all my cards from Apple Pay, my Amazon account, any other digital services. I don't want to give myself the opportunity or the chance to make an impulsive trade, an impulsive investment, or even spend my money thoughtlessly.

Create a system or environment where it's actually kind of hard to access your money. You want it to be hard to access your investments.

Maybe you only access your investment account at specific times of the month. Maybe you give someone you trust your passcode. Or you just make scheduled investments throughout the year and never log in otherwise.

2. Use the 72-Hour Rule

If you see something you want to buy or an investment you want to make, wait 72 hours. Three days. Then decide: do I still want to invest in that? Do I still want to do this?

This simple waiting period cuts through the urgency and status cues that drive bad decisions.

3. Choose Boring Platforms on Purpose

Use platforms with friction. Schwab, Fidelity, Vanguard - they're not sexy investing platforms, but that's the point. The boring interface is a feature, not a bug.

Visual representation of a Charles Schwab brokerage. It's low-key boring, but it's still simple enough where it doesn't create dopamine hits in addiction.

But Is Personal Discipline Enough?

Here's where I have to be honest: is personal discipline enough when systems are designed to exploit you?

Should Robinhood be allowed to use confetti animations? Should there be cooling-off periods built into platforms? Should options trading require some kind of licensing or education requirement?

If you have time, be sure to check out this book because you start to realize that money is more so emotional than it is strategic.

I don't have all the answers, but I know this: we can't just tell people to "be smarter" when the entire ecosystem is engineered to take advantage of behavioral psychology.

35 states now require high school students to take a personal finance course. That's a start. But is it enough when the apps are designed by teams of PhDs in behavioral economics whose entire job is to maximize engagement?

Living in a capitalist society is great because it allows the best ideas to thrive. But on the consumer end, you have to do your own due diligence. You must educate yourself.

What Actually Matters

So here's where we land:

The tools are more powerful than ever. The casino is louder than ever. The pressure is heavier than ever.

But what actually matters hasn't changed.

Building wealth is still about income minus expenses, and investing that difference over a long time. That's it. That's the boring truth everyone wants to ignore.

You can only decrease expenses so much. There's a floor. But there are always more opportunities to increase your income than cut your spending - a new skill, a side project, a promotion, a career change.

Yes, the tools are there. Yes, you can open an account in three minutes. But here's the real question: do you understand yourself well enough to use them properly?

Because personal finance is personal. What works for The Daily Driven Porsche doesn't work for me. What works for me might not work for you. And that's okay.

The point isn't to find the perfect strategy. The point is to find your strategy - and then stick to it long enough to see it work.

Focus on the fundamentals. Build systems that protect you from yourself. Avoid the noise. Don't chase the TikTok millionaires.

The casino is open 24/7.

But you don't have to play.

Because unlike the casino, when you stick to the boring fundamentals, you'll actually win.

Luv,

Luv